*NECO ACCOUNTING*

ACCOUNTING OBJ

01-10: CEDEAEDBCC

11-20: EDAEDBDEAD

21-30: BDCDADDDEE

31-40: BBDEBBCBBD

41-50: BACAABABBE

51-60: CEBEBDDCEC

=============

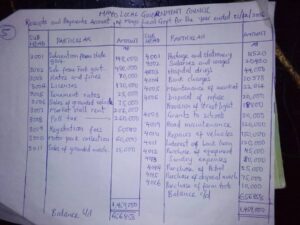

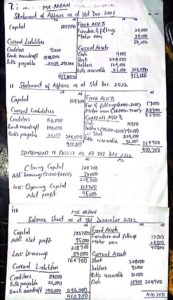

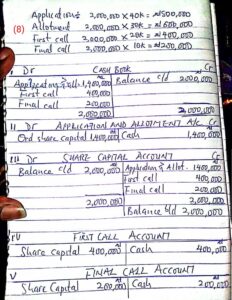

NECO GCE FINANCIAL ACCOUN

(1)

(i) General Warrant: A General Warrant is a legal document issued by the government that authorizes the withdrawal of funds from the Consolidated Revenue Fund or other designated funds to meet specified expenditures. It is usually issued at the beginning of the financial year and serves as a blanket authority for expenditures.

(ii) Capital Expenditure: Capital Expenditure refers to government spending on assets that have a useful life of more than one year, such as buildings, roads, bridges, and equipment. These expenditures are typically financed through borrowing or from the government’s capital budget.

(iii) Recurrent Expenditure: Recurrent Expenditure refers to government spending on goods and services that are consumed within a short period, typically within a year. Examples include salaries, wages, utilities, and maintenance costs. These expenditures are usually financed from the government’s recurrent budget.

(iv) Supplementary Budget: A Supplementary Budget is an additional budget presented by the government during the financial year to request additional funds or to reallocate existing funds. This is usually done to address unforeseen expenditures or changes in economic conditions.

(v) Payment Voucher: A Payment Voucher is a document that authorizes the payment of a specific amount to a supplier, contractor, or employee. It contains details such as the date, amount, and description of the payment, as well as the accounting codes and budget line items. Payment vouchers serve as a control mechanism to ensure that payments are properly authorized and recorded.

=========

(2a)

(PICK ANY FIVE)

(i) Names and addresses of the partners.

(ii) Capital contributions of each partner.

(iii) Profit-sharing ratio among partners.

(iv) Rights and duties of the partners.

(v) Procedure for admitting new partners or retiring existing ones

(vi) Method for resolving disputes among partners.

(vii) Duration of the partnership or conditions for dissolution.

(vii) Rules regarding the withdrawal of capital by partners.

(2b)

(i) Accrual refers to the accounting principle that recognizes revenues and expenses when they are earned or incurred, regardless of when cash is received or paid. This means that revenues are recorded when earned, and expenses are recorded when incurred, even if the payment has not been made yet.

(ii) Prepayment refers to a payment made in advance for goods or services that will be received in the future. In accounting, prepayments are recorded as assets until the goods or services are received, at which point they are expensed.

(iii) Provision for bad debt, also known as allowance for doubtful accounts, is an accounting entry that represents the estimated amount of accounts receivable that are unlikely to be collected. This provision is made to recognize that some customers may default on their payments, and it helps to match the expense with the related revenue.

(3)

(i) Goodwill: Goodwill refers to the excess amount paid by a company to acquire another company or business over its net asset value. Goodwill represents the value of intangible assets such as reputation, brand name, customer loyalty, and patents.

(ii) Bad debt: This refers to an account receivable that is unlikely to be collected due to a customer’s inability or refusal to pay. Bad debts are typically written off as an expense against the company’s profits.

(iii) Preference share: This is a type of share that has a higher claim on assets and dividends than ordinary shares. Preference shareholders have a priority claim on dividends and assets, but they usually do not have voting rights.

(iii) Depreciation: This is the systematic allocation of the cost of a tangible asset over its useful life. It represents the decrease in value of an asset due to wear and tear, obsolescence, or other factors.

(iv) Accumulated fund: This refers to the portion of a company’s profits that are reinvested in the business rather than being distributed as dividends to shareholders.

Leave a Reply